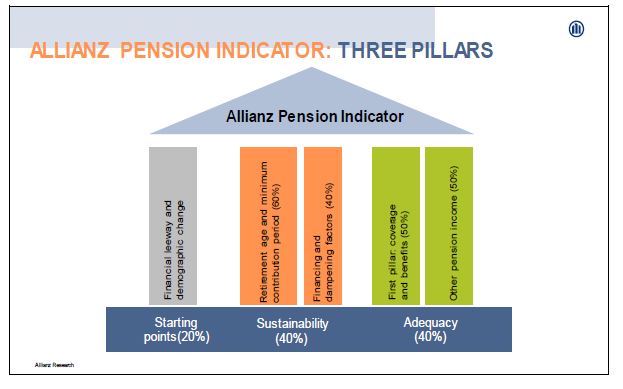

Allianz unveiled the first edition of its "Global Pension Report", taking the pulse of pension systems around the world with its proprietary pension indicator, the Allianz Pension Indicator (API). The indicator follows a simple logic: It starts the analysis with the demographic and fiscal prerequisites and then continues to examine pension systems along their two decisive dimensions: sustainability and adequacy. Hence, it is based on three pillars and takes all in all 30 parameters into account, which are rated on a scale of 1 to 7, with 1 being the best grade. By adding up all weighted subtotals, the API assigns each of the analysed 70 countries a grade between 1 and 7, thus providing a comprehensive view of the respective pension system.

With a higher life expectancy today, it is only consequential that the worldwide number of people in retirement age is set to more than double within the next 30 years from 728mn to 1.5bn in 2050. In many emerging economies, the number is going to more than double within the next 30 years.

The three pillars of API

Source: Allianz Global Report 2020

The first pillar of API combines demographic change and the public financial situation (financial leeway). Emerging countries in Africa score well as the population is still young and public deficits and debts are low. Whereas many European countries are among the worst performers: Old populations meet high debts.

The second pillar of the API is sustainability, measuring how systems react to demographic change: Are there built-in stabilisers or will the system be blown apart when the number of contributors falls while that of beneficiaries keeps rising? In that context, an important lever is the retirement age.

In the 1950s, an average 65-year old men, living in Asia could expect to spend around 8.9 years in retirement, with the average women 10.3 years. Today, the average further life expectancy of a 65-year old is 17.8 years for women and 15.2 years for men and it is set to increase to 19.9 years (women) and 17.5 years (men) respectively in 2050.

As a consequence, the ratio of working life to time spent in retirement has declined markedly. Countries which decided to adjust the legal retirement age or the increase of pension benefits to the development of further life expectancy like the Netherlands, have thus a more sustainable pension system than countries where postponing retirement further is still a taboo.

The third pillar of the API rates the adequacy of a pension system, questioning whether it provides an adequate standard of living in old age. Important levers are the coverage ratio – i.e. how big are the shares of the working age population and the age group in retirement age that are covered by the pension system? –, the benefit ratio – i.e. how much money (measured in terms of average income) does an average pensioner receive? –, and last but not least the existence of capital-funded old-age provision and other sources of income.

Overall, the average score in the adequacy pillar (3.7) is slightly better than that in the sustainability pillar (4.0), a sign that most systems still put greater weight on the well-being of the current generation of pensioners than on that of the future generation of tax and social contribution payers. The countries leading the adequacy ranking have either generous state pensions, like Austria or Italy, or strong capital-funded second and third pillars, like New Zealand or the Netherlands.

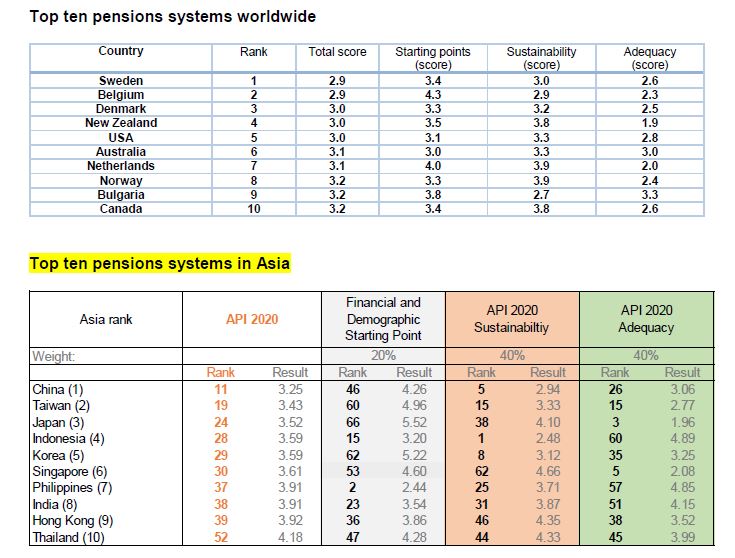

Where does Asia stand?

Source: Allianz Global Report 2020

There is no Asian market among the top-10. The Asian region has a high number of older population with only a few exceptions (India, Laos, and the Philippines). Countries in Asia are taking action against the backdrop of rapid aging. For example, China and Indonesia have decided to raise the retirement age significantly. Four markets, China, Japan, South Korea, and Taiwan have already included a demographic factor in their pension formula. As a result, Indonesia, China, and South Korea are among the top-10 in the sustainability rankings.

Singapore and Japan, on the other hand, boast a wide coverage in their first pillar and built a strong second pillar; thus, both markets rank among the top-5 in the adequacy ranking. Overall, currently, China’s pension system is the best-prepared for the upcoming demographic change, ranking at #11 on the global list. But most other Asian markets have still homework to do to make their systems demography-proof.

You can find the full study here.

For more articles on retirement:

Singapore: 46% of residents expect their family will look after them in retirement.

A Possible Solution to the Soaring Old-Age Dependency Ratio?

What are your parents' financial plans? - Kenny Tey

For the full suite of stories and updates, always check in to our Facebook / LinkedIn. Click the following if you want to improve your sales, learn how to be a better leader, or you just need some motivation to kick start your engine.

Do you have a new product or programme to share? Or perhaps you are keen to explore any collaborations with us or our partners? Reach out to us at Connect@AsiaAdvisersNetwork.com